Can You Buy With a 5% Deposit and No LMI in Australia? 5% Deposit Scheme Explained (June 2026 Update)

Can eligible first home buyers in Australia still buy with a 5% deposit and no LMI? Here’s how the Australian Government 5% Deposit Scheme works in June 2026, what changed from the old First Home Guarantee, and what to check before applying.

Buying your first home in Australia is confusing enough without the paperwork. Throw in a 5% deposit scheme, no LMI, property price caps, a list of "participating lenders", and people still talking about "35,000 places" like it is still the old scheme — and it is easy to wonder whether any of it still applies to you.

I went down this same rabbit hole myself a while back, trying to work out whether this was a grant, a discount, or just a different way of structuring a home loan. It turns out it is not really any of those things. It is a government guarantee, and if you qualify, it may help you buy sooner without paying Lenders Mortgage Insurance.

So here is where things actually stand as of June 2026: how the scheme works now, who it is for, and what is worth checking before you sit down with a lender.

This matters whether you are buying alone, buying with a partner, or you are a single parent looking at the 2% deposit option. It can also matter if you are trying to use the First Home Super Saver Scheme or state-based first home buyer support at the same time.

Housing policy comes with a lot of numbers thrown around loosely, so this article keeps the focus on what you would actually need to do next.

Short answer first

Yes, eligible first home buyers may be able to buy with a 5% deposit and avoid Lenders Mortgage Insurance under the Australian Government 5% Deposit Scheme, depending on their circumstances.

The old "35,000 First Home Guarantee places" wording needs an update. That number belonged to the earlier Home Guarantee Scheme settings. From 1 October 2025, the program was expanded and renamed the Australian Government 5% Deposit Scheme.

As of June 2026, the official information says the scheme has no income caps, no waitlists and no LMI for eligible applicants.

That does not mean everyone is automatically approved. You still need to apply through a participating lender. The lender checks you, the property and the loan against the scheme rules. They also assess whether you can actually afford the loan.

The scheme does not give you cash. It does not pay your deposit for you. It is not something you claim in your tax return. You are still responsible for your deposit, stamp duty where it applies, conveyancing, inspections, legal fees, loan repayments and ongoing home ownership costs.

The benefit is that Housing Australia provides a guarantee to the lender. If your application is approved under the scheme, that guarantee may allow the lender to waive LMI even though your deposit is below 20%.

You can check the current details on the official Australian Government 5% Deposit Scheme page.

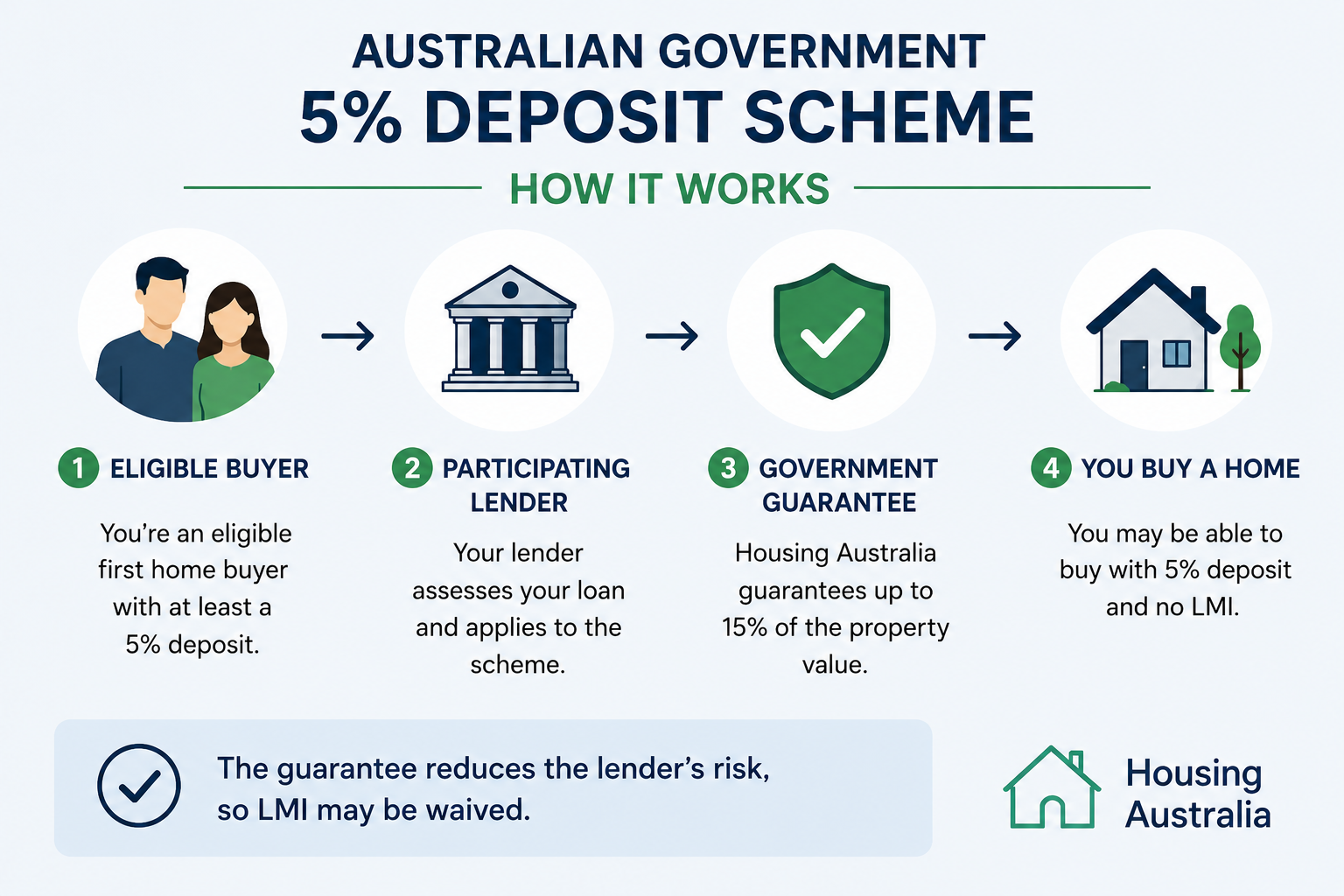

How the 5% Deposit Scheme Actually Works

The official name now is the Australian Government 5% Deposit Scheme.

Before October 2025, the broader program was known as the Home Guarantee Scheme, and the first home buyer stream was commonly called the First Home Guarantee. That is where the "35,000 places" wording came from, and why you still see it floating around in older articles.

Housing Australia runs the scheme on behalf of the Australian Government.

Here is the basic idea. If you buy a home with less than a 20% deposit, a lender may usually charge Lenders Mortgage Insurance. LMI protects the lender, not the buyer. It can add a significant upfront cost, depending on the property price, loan size, deposit and lender.

Under the 5% Deposit Scheme, Housing Australia guarantees part of the loan to the participating lender. Because part of the lender's risk is covered by the guarantee, the lender may be able to waive LMI for eligible applicants.

For a first home buyer, you generally need:

- a minimum 5% deposit

- a home you intend to live in, not an investment property

- Australian citizenship or permanent residency

- to be at least 18 years old

- a loan through a participating lender

- a property that sits within the relevant price cap

The guarantee can cover up to 15% of the property value. This is what allows a lender to consider a loan with a 5% deposit without charging LMI, if everything else checks out.

One thing worth knowing is that you cannot apply to Housing Australia directly. Your lender or broker handles the scheme application as part of the home loan process. If your lender is not participating in the scheme, you cannot access the scheme through that lender.

The big shift happened on 1 October 2025, when the income caps and annual place limits were removed. As of June 2026, there is no annual cap on how many eligible buyers can use the scheme, but you still need to meet the other rules.

If you want a first check before speaking with a lender, the 5% Deposit Scheme Eligibility Checker is worth using. It is only a guide, though. Your lender makes the final call.

Why the old 35,000 places wording is confusing

This is the part that catches a lot of people.

For the 2025–26 financial year, older scheme information referred to 35,000 First Home Guarantee places. Under the previous settings, places were limited each year, and buyers often had to ask whether their lender still had places available.

That changed from 1 October 2025.

The current Australian Government 5% Deposit Scheme is no longer best explained as a limited annual "35,000 places" scheme. Current official information says eligible buyers can access the scheme with no income caps and no waitlists, as long as the scheme rules are met.

So if you see an article saying there are only 35,000 places, check when it was written and whether it was updated after October 2025.

A simple way to remember it is this:

- "First Home Guarantee" is the older name many people still recognise.

- "35,000 places" refers to the earlier allocation.

- "Australian Government 5% Deposit Scheme" is the current official name.

- Your lender should assess you under the current rules, not an old article.

That does not mean the scheme is open without conditions. It simply means the old "limited places" framing is not the most accurate way to understand the scheme in June 2026.

Property price caps and where you can buy

Property price caps are one of the most important checks, and they can be easy to overlook.

The scheme does not apply to every property. The home must be within the relevant price cap for its location. A capital city cap may be different from a regional cap, and the cap can vary by state or territory.

The scheme may apply to different residential property types, including:

- an existing house

- a townhouse

- an apartment

- a house and land package

- vacant land with a building contract

- an off-the-plan purchase

If the property sits above the relevant cap, even by a small amount, it may not qualify under the scheme. For new builds, the combined land and build cost may also matter.

It is not only the listing price you should think about. In practice, lenders may also consider valuation and loan details when assessing eligibility. This is why it is better to check early, before you spend money on reports, contract review or other buying costs.

Before you get too attached to a particular listing, check the official Property Price Caps page and confirm the details with your lender.

Who actually qualifies?

In plain English, the scheme is mainly for eligible first home buyers, and also for some buyers who have not owned property in Australia for at least 10 years.

You need to be buying a home to live in. Investment properties are not the point of this scheme. You also need to apply through a lender that participates in the program.

For first home buyers, the minimum deposit is 5%. For eligible single parents or legal guardians, there is a separate 2% deposit pathway. If that applies to you, it is worth asking the lender which pathway is better for your circumstances.

Eligibility is not just about the buyer. The property, loan type and lender approval all matter too.

To give yourself the best shot, you want at least a 5% deposit saved, a property sitting under the relevant price cap, and a lender who is actually participating in the scheme. Beyond that, the lender will look at your income, expenses and overall loan application the same way they would for any home loan — the scheme does not change that part of the process. Having your paperwork sorted before you make an offer tends to help more than people expect.

You can check the current list of participating lenders on the 5% Deposit Scheme Participating Lenders page.

How the First Home Super Saver Scheme may fit in

The First Home Super Saver Scheme, often called FHSS, is separate from the 5% Deposit Scheme. It is run through the Australian Taxation Office.

FHSS allows eligible first home buyers to make voluntary contributions into super and later apply to release eligible amounts, plus associated earnings, to help buy or build a first home.

Some buyers may use FHSS money as part of their deposit and still apply for the 5% Deposit Scheme through a participating lender. That can be useful if you have been saving through super and want to put those released funds toward your deposit.

The timing is the part to watch. FHSS has steps that need to happen in the right order. You generally need to request a determination and follow the ATO release process. It is not something to leave until the week before settlement.

You can read the official process on the ATO's First home super saver scheme page.

How the two schemes compare

The short version: these are two completely different programs that happen to work toward the same goal.

The 5% Deposit Scheme does not put money in your account. Housing Australia provides a guarantee to the lender, which may let the lender waive LMI if everything else qualifies. You are still borrowing the full loan amount. FHSS works differently — it is about releasing money you have already saved inside super, through an ATO process, and using that toward your deposit.

Neither is automatic, and neither replaces the other. If you have been putting voluntary contributions into super for a few years, FHSS might give you a bigger deposit to work with. The 5% Deposit Scheme might then let you avoid LMI even if that deposit is still under 20%. Whether both apply to your situation depends on the specifics.

Eligibility works differently too. For the 5% Deposit Scheme, the lender checks your buyer status, deposit, property and loan type. For FHSS, the ATO checks your voluntary super contributions and release eligibility. You can look up both on their respective official pages — the Australian Government 5% Deposit Scheme and the ATO's First home super saver scheme page.

So when does this actually help?

This scheme is most useful when you have a deposit, but not a 20% deposit.

For example, you might have enough saved for 5% of a property within the price cap, but waiting until you reach 20% could take years. In that situation, the scheme may help you avoid LMI and buy sooner, if the lender approves the loan.

It can also help buyers who have been paying rent while trying to save. Rent, groceries, insurance, childcare, transport and other costs can make saving a large deposit feel slow. The scheme does not solve every problem, but it may remove one major upfront barrier.

The situations where it tends to actually make a difference: you have 5% saved, the property is under the cap, you plan to live in it, and your borrowing capacity holds up when the lender runs the numbers. If you can also stack state-based support — a First Home Owner Grant or stamp duty concession, depending on where you buy — that can reduce the upfront cost further. Those are separate programs though, so check what your state or territory offers before assuming anything applies.

It is less likely to help if the property is above the cap, you are buying an investment property, your borrowing capacity is not strong enough, or you are relying on money that has not yet been released or confirmed.

In NSW, for example, you can start with the Revenue NSW — First home buyer assistance page.

A few things to watch for

The first mistake is relying on old information about the 35,000 places figure. If a page still talks about limited places or income caps, check whether it was updated after the October 2025 expansion.

The second mistake is overlooking property price caps. A property can look suitable online, but still fail the scheme rules if it sits above the relevant cap or does not meet the lender's requirements. Before making an offer, check the cap and ask your lender to confirm how it applies.

The third mistake is assuming no LMI means easy loan approval. The bank still assesses your loan. Credit cards, personal loans, HECS or HELP debt, car finance, living expenses and interest rate buffers can all affect borrowing capacity.

The fourth mistake is forgetting the other buying costs. Even if LMI is waived, you may still need money for conveyancing, inspections, insurance, moving costs, rates, strata fees, repairs and stamp duty where it applies.

If you are relying on FHSS money, timing is another risk. Check the ATO process early and do not assume funds will be released in time unless you have followed the steps correctly.

How to check

The official Australian Government 5% Deposit Scheme page is the right place to start. Read the current rules and run through the 5% Deposit Scheme Eligibility Checker before you do anything else — it only takes a few minutes and gives you a rough sense of whether you are in the right ballpark.

Then check the 5% Deposit Scheme Participating Lenders list. Not every lender is part of the scheme, so it is worth checking before you get too far into the loan process.

When you speak to a lender or broker, ask:

- "Are you a participating lender for the Australian Government 5% Deposit Scheme?"

- "Can you assess my eligibility before I make an offer?"

- "Does this property fall under the current price cap?"

- "How do you treat the bank valuation for the scheme?"

- "What documents do you need specifically for the scheme?"

- "Will my loan documents show whether LMI has been waived?"

When you are looking through pre-approval or loan documents, search for phrases such as:

- "LMI"

- "Lenders Mortgage Insurance"

- "Housing Australia guarantee"

- "5% Deposit Scheme"

- "price cap"

- "owner-occupier"

- "valuation"

- "principal and interest"

If FHSS is part of your plan, log into myGov and go to ATO online services. Look for super, voluntary contributions, FHSS determination and release request information. The ATO explains the process on its First home super saver scheme page.

For state-level help, go to your state or territory revenue office. In NSW, check Revenue NSW — First home buyer assistance. Other states and territories have their own grant, duty and concession pages.

It is worth keeping a folder with your lender emails, eligibility check results, savings records, ATO information, contract documents and state grant or duty concession details. When more than one program is involved, having the paperwork together makes it easier to see what has actually been confirmed.

The bottom line

The "35,000 First Home Guarantee places" framing is now out of date. As of June 2026, the program to check is the Australian Government 5% Deposit Scheme.

The main benefit is straightforward: eligible buyers may be able to buy with a 5% deposit and avoid LMI, if the scheme rules are met and the lender approves the loan.

It is not a cash payment. It is not automatic. It is not something you claim at tax time. It works through a government guarantee to the participating lender.

You may also be able to combine it with FHSS savings or state-based first home buyer support, depending on your situation. Each program has its own rules and timing.

Most of these options require you to ask, search or apply first. Rules, caps and lender lists can change, so it is worth checking the official website or confirming with your lender before making decisions based on your own situation.

Sources

- First Home Buyers — Australian Government 5% Deposit Scheme

- First Home Buyers — First home buyers

- First Home Buyers — 5% Deposit Scheme Eligibility Checker

- First Home Buyers — Property Price Caps

- First Home Buyers — 5% Deposit Scheme Participating Lenders

- Australian Taxation Office — First home super saver scheme

- Revenue NSW — First home buyer assistance