How Much Tax Will You Actually Get Back in Australia? ($50k, $80k, $120k and $150k Compared, 2025–26)

Compare realistic Australian tax refund examples for $50k, $80k, $120k and $150k salaries using 2025–26 ATO rates, including deductions, Medicare levy and common refund mistakes.

If you have ever lodged your tax return and thought, “Wait, is that actually right?” you are not alone.

Tax refunds can feel confusing. One person gets a few thousand dollars back. Another person on a similar salary gets almost nothing. Someone else lodges their return and ends up with a tax bill instead.

I had the same question at first, especially when trying to work out whether a refund amount made sense or whether something had been missed.

Today, we are looking at what a realistic tax refund could look like across four common salary levels in Australia: $50,000, $80,000, $120,000 and $150,000, using 2025–26 financial year examples.

This is not a one-size-fits-all answer. Your refund depends on several moving parts: how much tax was withheld from your pay, whether you have valid deductions, whether you qualify for offsets, and whether extra items such as HELP debt, investment income or Medicare levy surcharge apply.

But this comparison should give you a practical starting point.

Whether you are a full-time employee checking your PAYG withholding, someone trying to understand why your refund changed, or simply planning ahead before lodging, this guide explains the key things to know.

Short answer first

Your tax refund is not a bonus.

It is the difference between what you actually owe and what has already been taken out of your pay during the financial year.

If your employer withheld more tax than your final tax calculation requires, you may get a refund. If your employer did not withhold enough, or if you have extra income or other tax obligations, you may have to pay more.

Most salaried employees with no major deductions often end up with a small refund or close to zero, because PAYG withholding is designed to be reasonably accurate across the year.

Bigger refunds usually happen because of valid deductions, tax offsets, part-year work, changes in circumstances, or withholding differences.

You can check the current resident tax brackets directly on the ATO tax rates for Australian residents page.

What the tax brackets look like in 2025–26

Australia uses a progressive tax system. This means higher tax rates apply as your income increases, but only to the part of your income above each threshold.

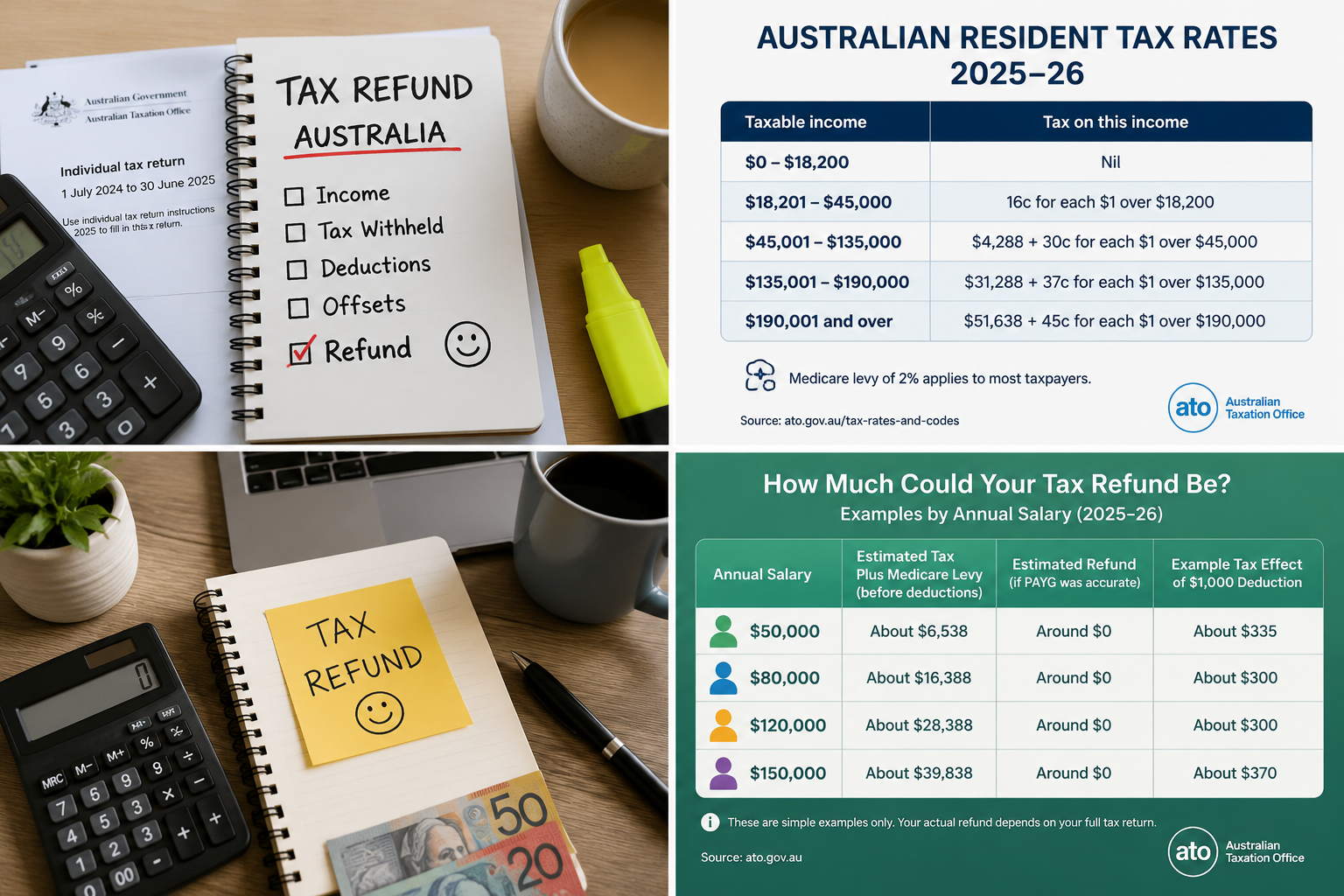

For the 2025–26 financial year, the Australian resident tax rates are:

- $0 to $18,200: Nil

- $18,201 to $45,000: 16 cents for each $1 over $18,200

- $45,001 to $135,000: $4,288 plus 30 cents for each $1 over $45,000

- $135,001 to $190,000: $31,288 plus 37 cents for each $1 over $135,000

- $190,001 and over: $51,638 plus 45 cents for each $1 over $190,000

These rates do not include the Medicare levy.

For many taxpayers, the Medicare levy is 2% of taxable income. Some people may qualify for a reduction or exemption depending on income and personal circumstances. The ATO explains this separately on the Medicare levy page.

The Low Income Tax Offset, often called LITO, can also reduce tax for eligible lower-income earners. You can read the official rules on the ATO Low income tax offset page.

One important note: the Low and Middle Income Tax Offset, known as LMITO, has ended. It should not be included as an active offset for 2025–26 tax refund estimates.

Salary-by-salary breakdown: what you might actually owe

The examples below are simple estimates only. They assume:

- You are an Australian resident for tax purposes

- You earn salary or wages from one employer

- You have no extra deductions

- You have no HELP or student loan repayment included

- You have no Medicare levy surcharge

- You have no investment, rental or business income

- You have no salary packaging adjustment

- You have no reportable fringe benefits

- You pay the standard 2% Medicare levy

- LITO is included where relevant

- Your employer withheld roughly the correct amount during the year

These examples are not personal tax advice. They are a practical way to compare how salary affects tax payable and why a refund may still be small even on a lower or higher income.

Salary-by-salary breakdown: what you might actually owe

The examples below are simple estimates only. They assume you are an Australian resident for tax purposes, earn salary or wages from one employer, have no extra deductions, no HELP debt, no Medicare levy surcharge, no investment income, and pay the standard 2% Medicare levy.

These examples are not personal tax advice. They are a practical way to compare how salary affects tax payable and why a refund may still be small even on a lower or higher income.

$50,000 salary

- Estimated income tax plus Medicare levy before extra deductions: about $6,538

- Estimated refund if PAYG withholding was accurate: around $0

- Example tax effect of a $1,000 valid deduction: about $335

- Example tax effect of $3,000 valid deductions: about $1,005

$80,000 salary

- Estimated income tax plus Medicare levy before extra deductions: about $16,388

- Estimated refund if PAYG withholding was accurate: around $0

- Example tax effect of a $1,000 valid deduction: about $300

- Example tax effect of $3,000 valid deductions: about $900

$120,000 salary

- Estimated income tax plus Medicare levy before extra deductions: about $28,388

- Estimated refund if PAYG withholding was accurate: around $0

- Example tax effect of a $1,000 valid deduction: about $300

- Example tax effect of $3,000 valid deductions: about $900

$150,000 salary

- Estimated income tax plus Medicare levy before extra deductions: about $39,838

- Estimated refund if PAYG withholding was accurate: around $0

- Example tax effect of a $1,000 valid deduction: about $370

- Example tax effect of $3,000 valid deductions: about $1,110

The key point is not that everyone on $150,000 gets a bigger refund. They do not.

If your employer withheld the right amount during the year, your refund may be close to zero, even on a higher salary. The table simply shows that deductions can have a different tax effect depending on the tax bracket your income sits in.

Someone on $150,000 with no deductions and accurate PAYG withholding may receive little or no refund. Someone on $80,000 with valid work-related deductions may receive a larger refund than someone earning much more.

At $50,000

At a salary of around $50,000, the Low Income Tax Offset may still be relevant.

Using a simple 2025–26 example, estimated income tax plus Medicare levy may be around $6,538 before extra deductions. If your employer withheld about the right amount during the year, your refund may be small or close to zero.

A larger refund may happen if you have valid deductions or if too much tax was withheld during the year.

Common areas to check may include work-related expenses, uniforms or protective clothing, union fees, professional registrations, tools, equipment or working-from-home expenses. But the expense must meet ATO rules, and you need records where required.

Before claiming anything, check the ATO’s official guide on deductions you can claim.

At $80,000

At around $80,000, the tax position is often fairly predictable for a straightforward employee.

Using the simple assumptions above, estimated income tax plus Medicare levy may be around $16,388 before extra deductions. If your PAYG withholding was accurate, your refund may be small.

This is the income level where many workers expect a refund because they may have work-related deductions. Examples could include professional memberships, work-related courses, home office costs, tools, protective equipment or union fees.

But again, the refund does not come from salary alone. It comes from the difference between tax withheld and final tax payable.

If you want to understand how your final return is calculated, the ATO gives an overview on the Your tax return page.

At $120,000

At around $120,000, a straightforward employee may have estimated income tax plus Medicare levy of about $28,388 before extra deductions.

The same rule still applies: if your employer withheld the correct amount, your refund may be small or close to zero.

At this level, it is worth paying closer attention to things that can change your final tax result. These may include HELP debt, investment income, salary packaging, reportable fringe benefits, private health insurance settings or spouse details.

If you have a HELP debt, your compulsory repayment may affect your final tax position. HELP repayment rules and thresholds can change, so check official guidance before relying on any estimate. StudyAssist explains recent HELP repayment changes on its Government announces changes to HELP debt repayments page.

At $150,000

At around $150,000, a simple estimate of income tax plus Medicare levy may be about $39,838 before extra deductions.

At this income level, deductions may have a larger tax effect because some income sits in a higher tax bracket. However, higher income can also bring extra tax considerations.

One important issue is the Medicare levy surcharge. This is different from the standard Medicare levy. It may apply if your income for Medicare levy surcharge purposes is above the relevant threshold and you do not have an appropriate level of private hospital cover.

You can check the current rules on the ATO’s Medicare levy surcharge income, thresholds and rates page.

If you have HELP debt, investment income, capital gains, rental income, salary packaging or reportable fringe benefits, the result can change again.

This is why two people earning $150,000 can still have very different outcomes at tax time.

Why a $1,000 deduction does not mean a $1,000 refund

This is one of the most common misunderstandings at tax time.

A deduction usually reduces your taxable income. It does not usually come back to you dollar for dollar.

For example, if you claim a valid $1,000 deduction and your marginal tax rate is 30%, the income tax saving may be around $300. If the Medicare levy effect is also relevant, the total effect may be slightly different.

That means a $1,000 deduction might improve your refund, but it does not usually increase your refund by $1,000.

The ATO also requires you to keep records for many deductions. Before claiming, it is worth reading the ATO’s guide to records you need to keep.

Here's the difference at a glance

- Who pays it

Your employer withholds PAYG tax from your wages and reports it to the ATO during the year. - Amount

The amount withheld depends on your income, pay cycle, tax file number declaration and whether you claimed the tax-free threshold. - Automatic or not

PAYG withholding is usually automatic for employees. Deductions are not automatic. You generally need to claim them in your tax return. - How it is paid

If you are entitled to a refund, it is usually paid into your nominated bank account after your tax return is processed. - Application needed

You do not separately apply for a normal tax refund. You lodge a tax return, and the ATO works out whether you receive a refund or have an amount payable. - Who is eligible

You may receive a refund if your tax withheld is more than your final tax payable. This can happen because of deductions, offsets, withholding differences, part-year work or other tax adjustments.

So when can you get a bigger refund?

The honest answer is: when your final tax payable is lower than the amount already withheld.

That can happen in several common situations.

First, you may have valid work-related deductions. These could include tools, equipment, professional registrations, union fees, compulsory uniforms, protective clothing, work-related training or home office expenses. The key test is whether the expense directly relates to earning your income, whether you paid for it yourself, and whether you were not reimbursed.

You can read the ATO’s official information on work-related deductions.

Second, you may have worked only part of the financial year. If tax was withheld as though you were earning that income all year, but you only worked for part of the year, you may have overpaid tax.

Third, you may qualify for a tax offset. The Low Income Tax Offset is one example for eligible lower-income earners.

Fourth, too much tax may have been withheld. This can happen if your payroll setup was not quite right, if you changed jobs, or if you did not claim the tax-free threshold when you were allowed to.

On the other hand, you may receive a smaller refund or a tax bill if not enough tax was withheld. This can happen with multiple jobs, side income, bank interest, investment income, capital gains, rental income, HELP debt or Medicare levy surcharge.

A few things to watch for

One common mistake is assuming your refund will be the same every year. If your circumstances changed, your return may look different. A new job, more overtime, unpaid leave, parental leave, working from home, private health insurance changes or investment income can all affect the result.

Another mistake is claiming expenses without proper records. The ATO can ask for evidence of deductions. If you are claiming vehicle use, home office hours, tools, equipment, work-related subscriptions or training, keep records that show what you spent and how the expense relates to your work.

A third mistake is forgetting income that did not have tax withheld. Bank interest, dividends, side income, freelance work, rental income and capital gains can all affect your tax result.

It is also worth checking whether your employer has finalised your income statement before lodging. The ATO explains how to check this on its Access your income statement page.

How to check

Before lodging your return, log in to myGov and check your ATO income statement.

Look for:

- Gross payments

- Tax withheld

- Allowances

- Salary sacrifice

- Reportable fringe benefits

- Superannuation information

- Whether the income statement is marked as tax ready

Then check your payslips or final pay summary. Search for words such as:

- PAYG withholding

- Tax withheld

- Gross income

- Allowances

- Salary packaging

- Reportable fringe benefits

- Superannuation

Next, gather deduction records. Depending on your job, this may include receipts, invoices, logbooks, professional registration fees, union fees, work-related subscriptions, home office records, donation receipts or tax agent invoices.

If you want a rough estimate before lodging, you can use the Moneysmart income tax calculator. It can help with broad planning, but it is not a substitute for your actual ATO tax return calculation.

If your situation is complicated, such as having investment income, multiple jobs, a business, rental property, capital gains, salary packaging or HELP debt, it may be worth speaking with a registered tax agent.

The bottom line

Your tax refund is not determined by salary alone.

A worker earning $50,000, $80,000, $120,000 or $150,000 could receive a small refund, a larger refund, no refund, or a tax bill depending on tax withheld, deductions, offsets, Medicare levy, HELP debt, private health insurance, investment income and other personal details.

If your employer withheld the right amount and you have no extra deductions, your refund may be close to zero. That can be completely normal.

If you have valid deductions or offsets, your refund may increase if you meet the conditions. But deductions are not automatic, and you should only claim expenses that meet ATO rules.

Before lodging, check your income statement, review tax withheld, gather records and confirm current rules on official websites.

Tax rules can change, so always check the ATO website or speak with a registered tax agent before relying on any estimate for your own situation.

Sources

- Australian Taxation Office — Tax rates: Australian residents

- Australian Taxation Office — Your tax return

- Australian Taxation Office — Access your income statement

- Australian Taxation Office — Medicare levy

- Australian Taxation Office — Low income tax offset

- Australian Taxation Office — Deductions you can claim

- Australian Taxation Office — Work-related deductions

- Australian Taxation Office — Records you need to keep

- Australian Taxation Office — Medicare levy surcharge income, thresholds and rates

- StudyAssist — Government announces changes to HELP debt repayments

- Moneysmart — Income tax calculator